For the person who has good credit and income but not enough money for the down payment on a home, their qualified retirement program could offer them some help. The rules are different depending on whether it is a 401(k), a Roth IRA or a traditional IRA.

Up to half of the balance of a 401(k) or $50,000, whichever is less, can be borrowed by the owner at any age for any reason without tax or penalty assuming the employer permits it. There can be specific rules for loans from 401ks that would determine the repayment; interest is usually charged but goes back into the owner’s account. You can consult with your HR department to find out the specifics.

Up to half of the balance of a 401(k) or $50,000, whichever is less, can be borrowed by the owner at any age for any reason without tax or penalty assuming the employer permits it. There can be specific rules for loans from 401ks that would determine the repayment; interest is usually charged but goes back into the owner’s account. You can consult with your HR department to find out the specifics.

A risk in borrowing against a 401(k) comes if your employment ends before the loan has been repaid. The loan may have to be repaid with as soon as 60 days to keep the loan from being considered a withdrawal and subject to tax and penalty. Even if you continue with the same employer, failure to repay the loan could be considered a withdrawal also.

Roth IRA owners can withdraw their contributions tax-free and penalty-free at any age for any reason because the contributions were made with post-tax income. After age 59 ½, earnings may be withdrawn as long as the Roth IRA have been in existence for at least five years.

Traditional IRAs have a provision for first-time buyers which include anyone who hasn’t owned a home in the previous two years. A person and their spouse, if married, can each withdrawn up to $10,000 from their traditional IRA for a first-time home purchase without incurring the 10% early-withdrawal penalty. However, they will have to recognize the withdrawal as income in that tax year. For more information, go to IRS.gov.

Another interesting fact about this provision is that the taxpayer making the withdrawal can help a relative includes children, grandchildren, parents and grandparents.

If you want more information to clearly understand the issues involved relative to your specific situation, talk to your tax professional or consult www.IRS.gov.

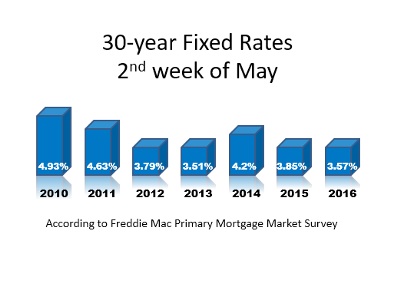

It is estimated that seven million out of 50 million homeowners could save money by refinancing their existing mortgages. Obviously, if the replacement mortgage has a lower rate than your existing one, you will save money.

It is estimated that seven million out of 50 million homeowners could save money by refinancing their existing mortgages. Obviously, if the replacement mortgage has a lower rate than your existing one, you will save money.